Your choice of retirement plan affects how much you can invest, save in taxes, incur in costs, and need to fund for employees each year. Taking just a little time upfront to understand your options will ensure you achieve your aims while averting unexpected consequences.

Your choice of retirement plan affects how much you can invest, save in taxes, incur in costs, and need to fund for employees each year. Taking just a little time upfront to understand your options will ensure you achieve your aims while averting unexpected consequences.

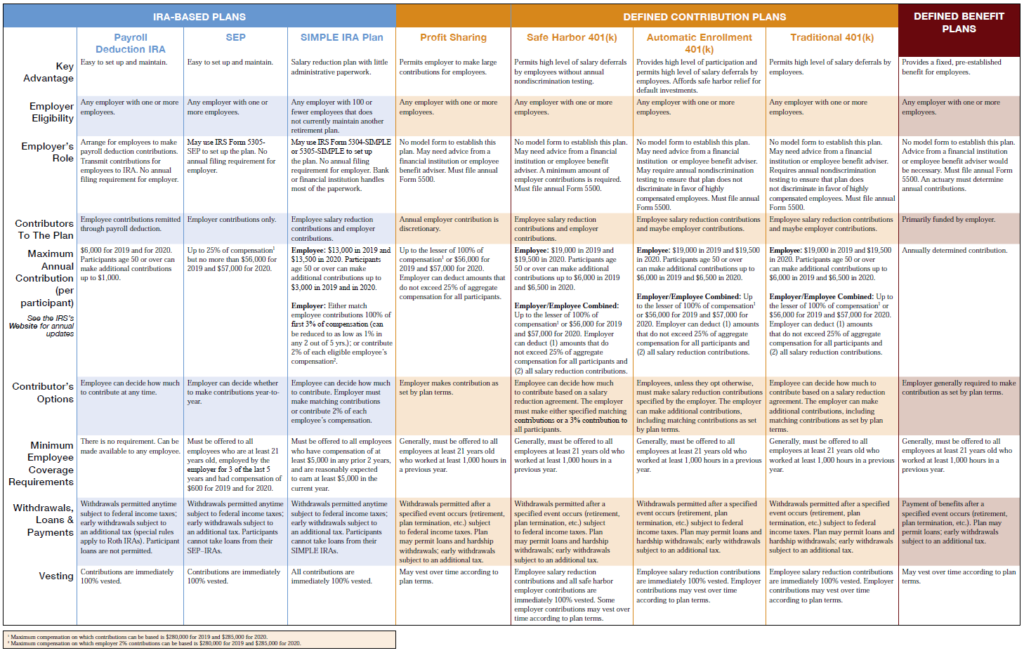

List of Small Business Retirement Plan Options

Almost all modern-day small business retirement plans fall under the category of “defined contribution plans” — This means they’re centered around how much can be put in (i.e., “contributed”). But before the age of defined contribution plans, “defined benefit plans” were the norm, and they’re centered around how much a person is entitled to take out (think “traditional pension”). There are still some special-use cases where defined benefit plans can make sense for specific entrepreneurs, but it’s not our goal to cover those here.

Among the defined contributions plans allowed by the IRS, there are:

- Payroll Deduction IRA: This isn’t really a company-sponsored retirement plan, but simply an option to allow employees to specify an amount to withhold from their paycheck towards their own Traditional/Roth IRA that the company then forwards to the financial institution. It essentially makes it easier for employees to save towards their own retirement and requires no financial overhead from the company.

- SEP IRA: Short for “Simplified Employee Pension”, SEPs are only funded with company contributions (i.e., employees do not have the option to contribute from their paychecks). The business can choose each year whether or not to make a SEP contribution (e.g., depending on profit/loss that year), but if a contribution is made it must be contributed at an equal percentage of compensation across all eligible employees. Eligibility can be defined as no more stringent than: Age 21, employed 3 of last 5 years at the company, and compensation of at least $600.

- SIMPLE IRA: SIMPLE IRAs are basically a simpler version of a 401(k) — It enables employees to contribute to their own accounts (up to $13,500 in 2020, with a $3,000 additional catch-up provision for those over 50), but it doesn’t come with the annual tax return and other compliance requirements of traditional 401(k)s. Part of the reason is because there’s a required company contribution equal to either 100% of an employee’s first 3% contributed, or a flat 2% of employee compensation regardless of employee contribution amount.

- Traditional 401(k): Most people are familiar with the concepts around 401(k)s which combine employee contributions ($19,500 max in 2020 with a $6,500 catch-up allowed for those over 50) and employer matching contributions. 401(k)s come with more flexibility around plan terms (like permitting loans) but also come with more regulatory requirements (like ensuring participation benefits are considered equitable among employees). As a result, they typically require an annual Form 5500 filing, non-discrimination testing, and more.

- Safe Harbor 401(k): Which is why the Safe Harbor 401(k) came about — It avoids many of the regulatory hoops of the Traditional 401(k) by requiring either a specified matching contribution or a 3% of compensation contribution to all participants. (An annual Form 5500 still has to be filed, it’s just simpler.)

- Solo 401(k): Yet another variant of the 401(k) is the Solo 401(k) (a.k.a., the “Individual 401(k)” or “One-participant 401(k)”, among others). As its name suggests, it’s only available to small businesses whose owner is the only employee of the business. And the main benefit of a solo plan is that, presuming you have enough business profit, you can very easily put large amounts of money into the plan as both the employee and the employer (e.g., $57,000 for 2020, or $63,500 for those 50 or older).

- Profit Sharing Plan: PSPs can either stand on their own or be combined with other plans (e.g., a common scenario is to pair with a 401(k)). Like it sounds, the gist of a PSP is to make a contribution to the plan each year (you can decide if and how much based on how the year went) and then have it shared with eligible employees according to a specified formula. Employer contributions on this and some of the other plans can be vested over defined periods.

There are a few other types of retirement plans that are less applicable to small business and which we’re not going to get into here (e.g., SARSEPs, Money Purchase Plans, 403(b)s, 457s, and ESOPs), but if you’re curious to learn more about these or additional details on the above plans check out the IRS’ page on Types of Retirement Plans.

We should also note that many of the above plans also exist in “Roth” form (e.g., a Roth 401(k)), so you often have the option of making both or one available if desired. (“Roth” variants mean employee contributions don’t reduce their taxable income, but do avoid tax when withdrawn.)

How to Choose the Retirement Plan for Your Small Business

Okay, so that’s a fair amount of groundwork, but what decides choosing one over the other? Usually that’s driven by the answer to key questions such as:

- Administrative complexity: Is the extra effort required around setting up and/or maintaining some of these plans too much of a hurdle and you’re simply looking for a way to direct money into retirement accounts? Then a Payroll Deduction IRA, SEP IRA, or SIMPLE IRA are likely a good fit for you.

- Desired contribution level: Do you have strong profits and are looking to put in $15,000k to $60,000+ each year? Then a SEP IRA, Solo 401(k), or Safe Harbor 401(k) paired with a Profit Sharing Plan are likely good candidates.

- Cash requirements: Would you prefer to flexibility to make contributions in good years, but not have minimum required company contributions if things are slimmer? Then a SEP IRA or stand-alone Profit Sharing Plan can do the trick. (Remember that certain plans will come with annual fees too, so that needs to be worked into your cash forecast.)

- Eligibility thresholds: Does your company have high turnover and/or you want to limit participation to team members that have been with you for a minimum amount of time? Then SEP IRAs or SIMPLE IRAs can be punch the ticket.

- Employee contributions: Alternatively, you may want to be sure employees can direct their own money to retirement, in which case SEPs and Profit Sharing Plans won’t work, while SIMPLEs and 401(k)s will. (Of course, keep in mind that employees are generally eligible to make personal IRA contributions even if the company doesn’t have its own plan.)

- Tax planning: Is the point to reduce your (or your employees’) taxable income now? Then the Roth variants aren’t going to do the trick, and plans with higher maximums (and especially large year-end discretionary company contributions) can empower flexible tax planning.

- Plan feature availability: How important is it to have the ability to take loans against account balances? How about to have company contributions vest over time? Or even hardship withdraw provisions? If these are very important, then the 401(k) variants are likely the road to go.

- Business identity: Last but certainly not least, how does retirement plan availability and type integrate with your business model, future plans, and company culture? This can be a tipping point when deciding between two plan options.

One other thing it’s important to know: Each plan has a different timeline for how short/long it is to get up-and-running (from essentially instant, to month or two), when the plan needs to be established to count for the current tax year, and when funds need to be transferred each year (and/or throughout the year). So if you know you want to make a move, it’s usually best to tackle in the first half of a tax year rather than its final month.

A Decision with Many Ripple Effects

The impact around if and which retirement plan to choose for your business are far-reaching and warrant more than a casual look before leaping. Our team at ElementsCPA guides entrepreneurs from the perspective that tax is only one part of your business and profit model — So it’s important to both know your numbers, and to think through the broader story of your business.

If this approach makes sense to you, we’d love to chat – Just reach out to our Design Team to arrange a Retirement Plan Comparison session, and let us confidently walk you through the right decision for your business.